Banking Cannabis: Why SAFE Still Matters After Schedule III

Why Does Cannabis Banking Still Feel Stuck In 2026?

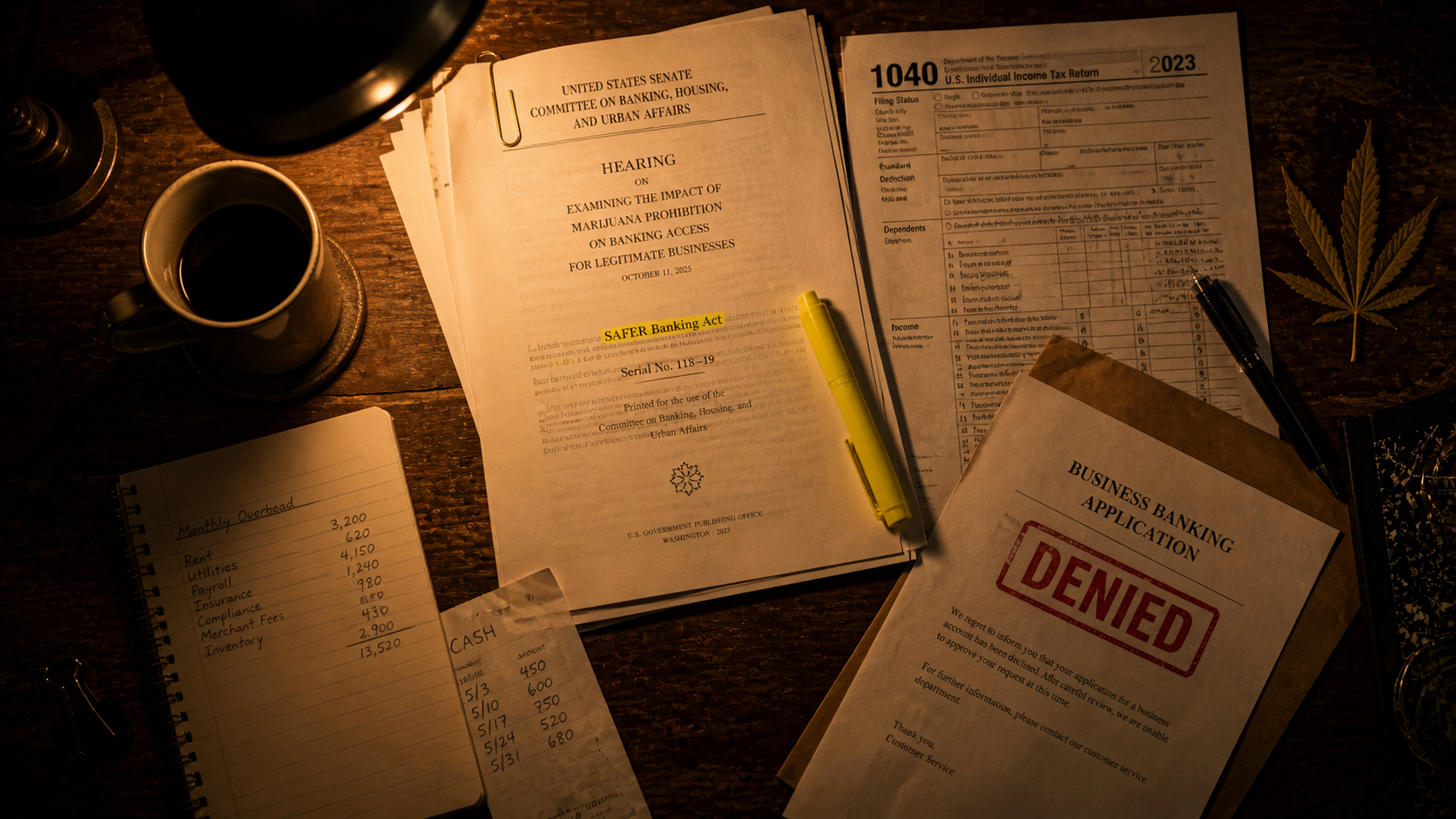

Cannabis banking still feels stuck in 2026 because rescheduling and banking are two different fights, and Congress only finished one of them. Trump's executive order moving cannabis from Schedule I to Schedule III cleared a giant tax and research barrier, but it did not, on its own, force a single bank or credit union to open an account for a state-licensed dispensary. The bill that would actually do that — the Secure and Fair Enforcement Regulation Banking Act, the current version of the older SAFE Banking Act — has not been refiled in the 119th Congress as of this writing. So the cash piles, the denied applications, and the armored-car runs are still part of the daily reality. That is the short answer. The longer answer is where it gets interesting.

What Did Schedule III Actually Change For The Industry?

Schedule III did real work. It opened the door for state-legal cannabis businesses to take normal federal tax deductions for the first time, which kills the choke-hold of IRS Section 280E that had been quietly bleeding operators for years. It also loosened research barriers around a plant that had been locked at Schedule I since 1970. Those are not small wins.

What it did not do is legalize cannabis federally. State-legal cannabis is still federally unlawful unless statutory exemptions or specific approval pathways are built. A March 2026 academic paper covered by [Marijuana Moment](https://www.marijuanamoment.net/marijuana-rescheduling-is-a-transitional-step-that-must-be-followed-by-banking-commerce-and-justice-reforms-new-analysis-says/) called Schedule III "transitional" and explicitly named banking, interstate commerce, and equity reforms as the work Congress still has to do. That framing matters because it sets the political ceiling honestly. Rescheduling is a foundation, not a finish line.

So Why Hasn't SAFER Banking Passed Yet?

Because the votes are not there yet, and the calendar keeps eating the clock. Per [Marijuana Moment's December 2025 reporting](https://www.marijuanamoment.net/gop-senator-says-marijuana-banking-bill-remains-stalled-but-trumps-rescheduling-order-could-spur-congress-to-act/), Sen. Bernie Moreno — expected to sponsor SAFER in the 119th Congress — said there have been "no" recent conversations about advancing the legislation. Sen. Steve Daines, the past lead GOP sponsor, has said colleagues "keep those opinions separate from SAFE Banking" even after the rescheduling order. Translation: the banking bill lives or dies on its own merits, not on the coattails of rescheduling.

The House has passed versions of cannabis banking reform seven times. The Senate has cleared it through committee. It has never reached a Senate floor vote. That is the wall, and it has been the same wall for almost a decade.

What Would SAFER Banking Actually Fix On The Ground?

It would stop federal regulators from punishing a bank or credit union for opening an account for a state-licensed cannabis business. That sounds narrow. It is not.

Right now, even if a small community bank in Nevada or California wants to take a dispensary's deposits, the federal exposure makes most institutions back away. So legitimate businesses run on cash. Cash is a robbery target, a money-laundering accusation waiting to happen, and a tax-compliance nightmare. SAFER Banking would let those banks serve cannabis businesses without fear of federal penalty, full stop. Per [Marijuana Moment's December 2025 Senate hearing coverage](https://www.marijuanamoment.net/bipartisan-senators-discuss-marijuana-industry-banking-issues-as-trump-strongly-considers-rescheduling/), Sen. Catherine Cortez Masto from Nevada was blunt about it: even with rescheduling, "that will not address the limits on banking services that are harmful for our Nevada cannabis growers and retailers."

A Congressional Budget Office analysis released around the one-year anniversary of the Senate committee passing SAFER projected billions of dollars in newly federally-insured cannabis deposits once banks get the protection. JPMorgan Chase's CEO has said publicly that the company "probably would" start banking cannabis if federal law allowed it. The plumbing is ready. The bill is the wrench.

Are There Any Backdoors Right Now?

A few. Per [Marijuana Moment's coverage of the CLIMB Act refile](https://www.marijuanamoment.net/marijuana-businesses-could-list-on-us-stock-exchanges-like-nasdaq-and-nyse-under-new-bipartisan-congressional-bill/), Reps. Guy Reschenthaler and Troy Carter refiled the CLIMB Act in March 2026, which would let cannabis businesses list on Nasdaq and the New York Stock Exchange and would shield service providers from punishment. That is a different angle on the same problem — opening the capital-markets door rather than the deposit-account door.

State-level momentum is also stacking up. Per [Marijuana Moment's April 2026 Hawaii reporting](https://www.marijuanamoment.net/hawaii-senate-votes-to-ask-congress-to-federally-legalize-marijuana/), the Hawaii Senate passed two resolutions by 20-5 votes asking Congress to deschedule cannabis, support state expungement efforts, and "facilitate access to the full spectrum of banking services for cannabis-related businesses." Resolutions are not laws. But they are the kind of pressure that gets a holdout senator's attention back home.

There has also been chatter, going back to 2025, about attaching cannabis banking language to other vehicles, including a stablecoin bill. None of that has materialized yet. But the industry has been here before. We covered the rescheduling fight in our prior post on [Schedule III federal cannabis reclassification](https://www.weedcoinog.com/schedule-iii-federal-cannabis-reclassification-explained), and the same dynamic applies — the policy moves when one piece finally finds the right vehicle to ride on.

Why Should I Care If I Don't Run A Dispensary?

Because cannabis banking is a stress test for whether a federal-state policy split can ever be patched without full descheduling. If SAFER passes, it is the first big proof that Congress can fix the seams of the cannabis economy without waiting for a constitutional showdown. If it stalls forever, every other half-measure on top of Schedule III gets weaker.

It is also a consumer-trust issue. State-legal businesses run on cash and that means more robberies, more compliance failures, more bad actors slipping through gaps that a real banking system would close. Banking access is, at the end of the day, a public-safety argument as much as a business one. Nobody in the conversation, even the GOP holdouts, denies that part.

FAQ

Q: Did Schedule III legalize cannabis?

No. It moved cannabis from Schedule I to Schedule III, which loosens tax and research rules but does not end federal prohibition.

Q: Is SAFE Banking the same as SAFER Banking?

SAFER is the current version. The old SAFE Banking Act got rebranded to SAFER as it was negotiated in the Senate. Most people still say "SAFE." It is the same fight.

Q: Has SAFER Banking been refiled in the 119th Congress?

Not as of this writing. Sen. Bernie Moreno is expected to sponsor it.

The bank account is still the wall. SAFER is still the wrench.

CONNECT WITH WEEDCOIN

Read the full post: https://www.weedcoinog.com/cannabis-banking-safe-act-after-schedule-iii-2026

Website: https://www.weedcoinog.com

Follow us on X: https://x.com/weedcoinog

Telegram: https://t.me/weedcoinogchannel

Chat With Wiz (GPT): https://bit.ly/ChatWithWeedcoin

Contract Address: 21nnfR4TkbZNLwvRrqEseAbz7P3kxKjaV7KuboLJpump

Like bitcoin but way higher 🌿